Cost Drivers Examples In Service Industry

A cost driver: • Is any factor whose change causes a change in the total cost of a related cost object. Hence a change in the level of cost driver will cause a change in the level of the total cost of a related cost object.

Examples of cost driver used in the following business units: • Research & Development:- Number of research projects, technical complexities of the projects • Design of products, services & process:- number of products in design, number of parts per product, • Marketing:- number of advertisement run, number of sales personnel, sales revenue • Distribution:-number of items distributed, number of customers, weight of items distributed • Customer services:-numbers of service calls, hours spent in servicing of products.

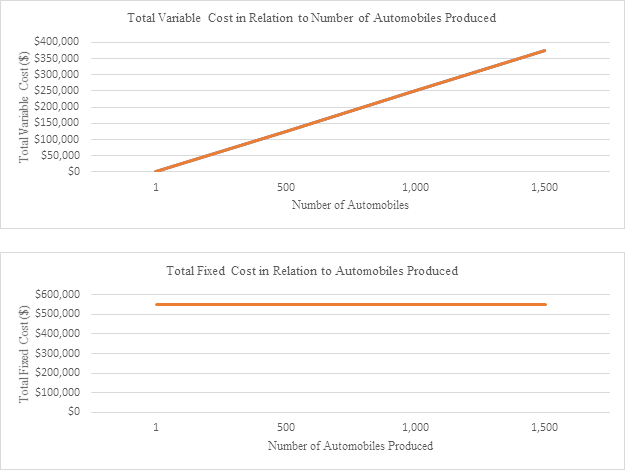

What is a Cost Driver? A cost driver is the direct cause of a Cost Structure Cost structure refers to the types of expenses a business incurs, and it is typically composed of fixed and variable costs. Fixed costs are costs that remain unchanged regardless of the amount of output a company produces, while variable costs change with production volume., and its effect is on the total cost incurred. For example, if you are to determine the amount of electricity consumed in a particular period, the number of units consumed determines the total bill for electricity. In such a scenario, the number of units of electricity consumed is a cost driver.

Application of a Cost Driver in Computing a Product’s Cost In a business venture, the major determinant of whether there will be continuity or discontinuity is cost. If the Product Costs Product costs are costs that are incurred to create a product that is intended for sale to customers. Product costs include direct material (DM), direct labor (DL) and manufacturing overhead (MOH). Understanding the Costs in Product Costs Recall that product costs include direct material, direct labor, and exceeds the revenue derived from a sale, there is a great probability of the business closing down. If the costs are less than Sales Revenue Sales revenue is the starting point of the income statement.

Time estimates as cost drivers. Are used as duration drivers to allocate resource costs to activities and cost objects. As the service industry grows in. TRADITIONAL APPROACH TO OVERHEAD. The present cost accounting systems, used almost universally in the United States, were developed over half a century ago. For this example, if the firm multiples total cost by 1.25 (a mark-up of 25% above total cost), then the average price of an audit engagement would be $46,724. Using a cost-driver approach, the firm would still allocate all of the direct costs of the engagements as shown in Table 2.

Islamic architecture 3d models free download. A propositional formula that helps you save time.

Sales or revenue is the money earned from the company providing its goods or services, income, there is profit and a probability of expansion. If the costs equal revenue, then the business is at a point of indifference and it can be closed or continued depending on other variables apart from cost or on how costs can possibly be adjusted. In order to make rational business decisions, you require viable costing methods to get the correct cost or a figure which is close enough to the actual cost for you to perform reliable cost/revenue analysis. Failure to do so can lead to the closing of a business venture, due to poor cost computation, that may actually be profitable, or at least potentially profitable.